Pipelines with auto_arima¶

Like scikit-learn, pmdarima can fit “pipeline” models. That is, a pipeline

constitutes a list of arbitrary length comprised of any number of

BaseTransformer objects strung together ordinally, and finished with an

AutoARIMA object.

The benefit of a pipeline is the ability to condense a complex sequence of

stateful transformations into a single object that can call fit,

predict and update. It can also be serialized into one pickle file,

which greatly simplifies your life.

Out:

pmdarima version: 0.0.0

Performing stepwise search to minimize aic

ARIMA(2,1,2)(0,0,0)[0] intercept : AIC=2819.938, Time=0.58 sec

ARIMA(0,1,0)(0,0,0)[0] intercept : AIC=2942.625, Time=0.03 sec

ARIMA(1,1,0)(0,0,0)[0] intercept : AIC=2867.514, Time=0.08 sec

ARIMA(0,1,1)(0,0,0)[0] intercept : AIC=2830.585, Time=0.31 sec

ARIMA(0,1,0)(0,0,0)[0] : AIC=2940.651, Time=0.12 sec

ARIMA(1,1,2)(0,0,0)[0] intercept : AIC=2817.535, Time=0.43 sec

ARIMA(0,1,2)(0,0,0)[0] intercept : AIC=2814.904, Time=0.36 sec

ARIMA(0,1,3)(0,0,0)[0] intercept : AIC=2818.704, Time=0.56 sec

ARIMA(1,1,1)(0,0,0)[0] intercept : AIC=2817.377, Time=0.33 sec

ARIMA(1,1,3)(0,0,0)[0] intercept : AIC=inf, Time=0.71 sec

ARIMA(0,1,2)(0,0,0)[0] : AIC=2815.283, Time=0.22 sec

Best model: ARIMA(0,1,2)(0,0,0)[0] intercept

Total fit time: 3.738 seconds

Model fit:

Pipeline(steps=[('fourier', FourierFeaturizer(k=4, m=12)),

('arima',

AutoARIMA(error_action='ignore', seasonal=False, trace=1))])

Forecasts:

[28518.74369032 29963.3967688 25827.07167847 25060.80502576

34235.82966664 33509.10289577 21083.2331318 19764.92917716

25895.83454266 25434.10945134]

[26536.11028356 34421.92193777 33695.1879951 21269.316609

19951.01751507 26081.9223959 25620.19457758 24414.29557272

26098.89428122 28871.66081912 30770.68308494]

print(__doc__)

# Author: Taylor Smith <taylor.smith@alkaline-ml.com>

import numpy as np

import pmdarima as pm

from pmdarima import pipeline

from pmdarima import model_selection

from pmdarima import preprocessing as ppc

from pmdarima import arima

from matplotlib import pyplot as plt

print("pmdarima version: %s" % pm.__version__)

# Load the data and split it into separate pieces

data = pm.datasets.load_wineind()

train, test = model_selection.train_test_split(data, train_size=150)

# Let's create a pipeline with multiple stages... the Wineind dataset is

# seasonal, so we'll include a FourierFeaturizer so we can fit it without

# seasonality

pipe = pipeline.Pipeline([

("fourier", ppc.FourierFeaturizer(m=12, k=4)),

("arima", arima.AutoARIMA(stepwise=True, trace=1, error_action="ignore",

seasonal=False, # because we use Fourier

suppress_warnings=True))

])

pipe.fit(train)

print("Model fit:")

print(pipe)

# We can compute predictions the same way we would on a normal ARIMA object:

preds, conf_int = pipe.predict(n_periods=10, return_conf_int=True)

print("\nForecasts:")

print(preds)

# Let's take a look at the actual vs. the predicted values:

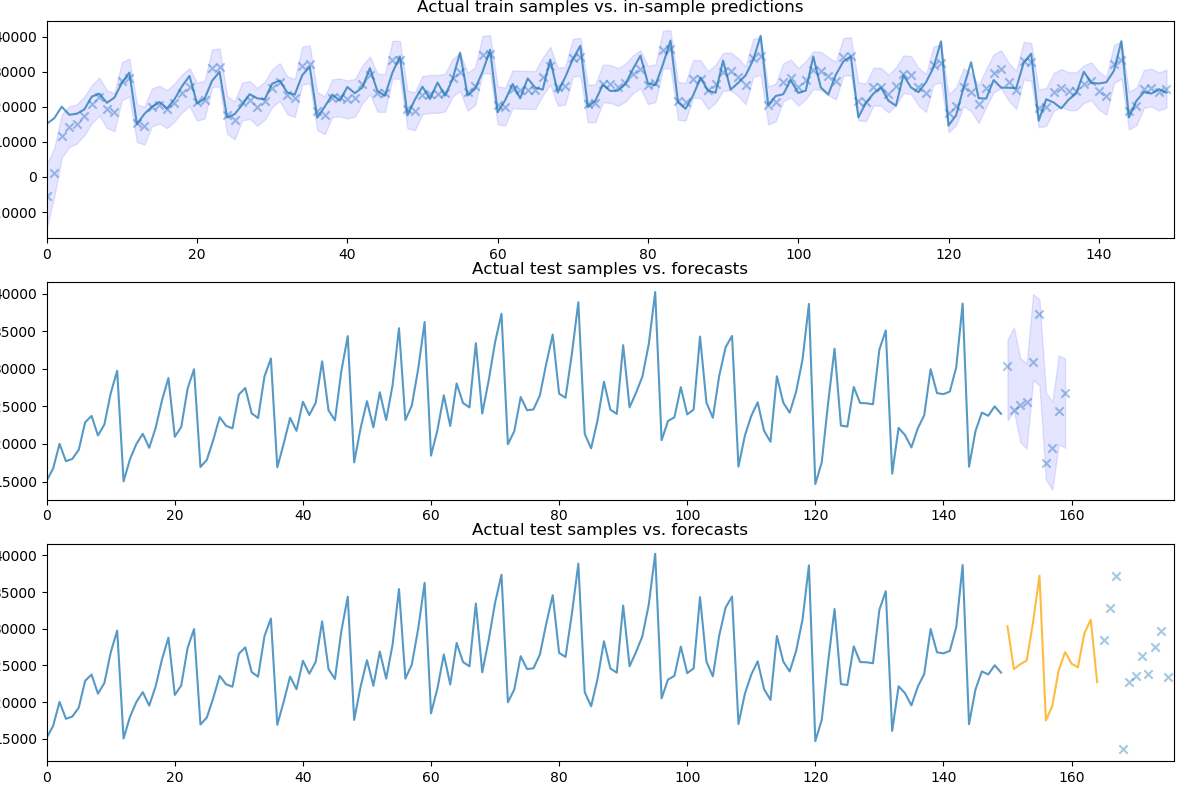

fig, axes = plt.subplots(3, 1, figsize=(12, 8))

fig.tight_layout()

# Visualize goodness of fit

in_sample_preds, in_sample_confint = \

pipe.predict_in_sample(X=None, return_conf_int=True)

n_train = train.shape[0]

x0 = np.arange(n_train)

axes[0].plot(x0, train, alpha=0.75)

axes[0].scatter(x0, in_sample_preds, alpha=0.4, marker='x')

axes[0].fill_between(x0, in_sample_confint[:, 0], in_sample_confint[:, 1],

alpha=0.1, color='b')

axes[0].set_title('Actual train samples vs. in-sample predictions')

axes[0].set_xlim((0, x0.shape[0]))

# Visualize actual + predicted

x1 = np.arange(n_train + preds.shape[0])

axes[1].plot(x1[:n_train], train, alpha=0.75)

# axes[1].scatter(x[n_train:], preds, alpha=0.4, marker='o')

axes[1].scatter(x1[n_train:], test[:preds.shape[0]], alpha=0.4, marker='x')

axes[1].fill_between(x1[n_train:], conf_int[:, 0], conf_int[:, 1],

alpha=0.1, color='b')

axes[1].set_title('Actual test samples vs. forecasts')

axes[1].set_xlim((0, data.shape[0]))

# We can also call `update` directly on the pipeline object, which will update

# the intermittent transformers, where necessary:

newly_observed, still_test = test[:15], test[15:]

pipe.update(newly_observed, maxiter=10)

# Calling predict will now predict from newly observed values

new_preds = pipe.predict(still_test.shape[0])

print(new_preds)

x2 = np.arange(data.shape[0])

n_trained_on = n_train + newly_observed.shape[0]

axes[2].plot(x2[:n_train], train, alpha=0.75)

axes[2].plot(x2[n_train: n_trained_on], newly_observed, alpha=0.75, c='orange')

# axes[2].scatter(x2[n_trained_on:], new_preds, alpha=0.4, marker='o')

axes[2].scatter(x2[n_trained_on:], still_test, alpha=0.4, marker='x')

axes[2].set_title('Actual test samples vs. forecasts')

axes[2].set_xlim((0, data.shape[0]))

plt.show()

Total running time of the script: ( 0 minutes 3.931 seconds)