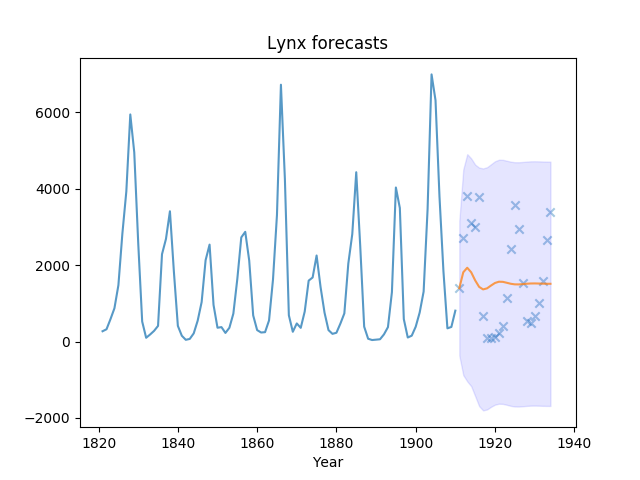

Fitting an auto_arima model¶

This example demonstrates how we can use the auto_arima function to

select an optimal time series model. We’ll be fitting our model on the lynx

dataset available in the Toy time-series datasets submodule.

Out:

Test RMSE: 1258.625

print(__doc__)

# Author: Taylor Smith <taylor.smith@alkaline-ml.com>

from pmdarima.datasets import load_lynx

from pmdarima.arima import auto_arima

from sklearn.metrics import mean_squared_error

import matplotlib.pyplot as plt

import numpy as np

# #############################################################################

# Load the data and split it into separate pieces

data = load_lynx()

train, test = data[:90], data[90:]

# Fit a simple auto_arima model

modl = auto_arima(train, start_p=1, start_q=1, start_P=1, start_Q=1,

max_p=5, max_q=5, max_P=5, max_Q=5, seasonal=True,

stepwise=True, suppress_warnings=True, D=10, max_D=10,

error_action='ignore')

# Create predictions for the future, evaluate on test

preds, conf_int = modl.predict(n_periods=test.shape[0], return_conf_int=True)

# Print the error:

print("Test RMSE: %.3f" % np.sqrt(mean_squared_error(test, preds)))

# #############################################################################

# Plot the points and the forecasts

x_axis = np.arange(train.shape[0] + preds.shape[0])

x_years = x_axis + 1821 # Year starts at 1821

plt.plot(x_years[x_axis[:train.shape[0]]], train, alpha=0.75)

plt.plot(x_years[x_axis[train.shape[0]:]], preds, alpha=0.75) # Forecasts

plt.scatter(x_years[x_axis[train.shape[0]:]], test,

alpha=0.4, marker='x') # Test data

plt.fill_between(x_years[x_axis[-preds.shape[0]:]],

conf_int[:, 0], conf_int[:, 1],

alpha=0.1, color='b')

plt.title("Lynx forecasts")

plt.xlabel("Year")

Total running time of the script: ( 0 minutes 1.355 seconds)